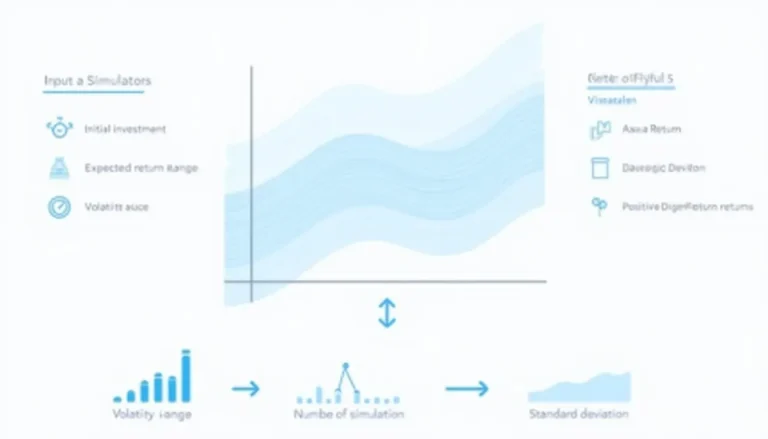

Portfolio Return Monte Carlo Simulator: Estimate Investment Outcomes

Unlock the power of data-driven investing with our Portfolio Return Monte Carlo Simulator. Explore thousands of potential scenarios, assess risks, and optimize your strategy. From beginners to pros, this tool empowers smarter financial decisions. Ready to revolutionize your investment approach? Dive in now!

Go toPortfolio Return Monte Carlo Simulator: Estimate Investment Outcomes